UnionBank July Inflation Report

Economy

364 week ago — 3 min read

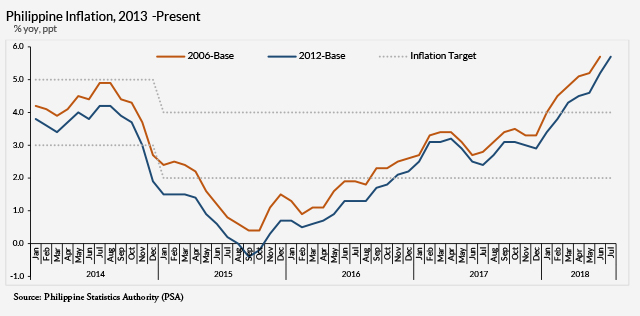

July inflation further accelerated to 5.7%. Inflation last month was observed at 5.2%, highest in five years, and 2.4% in the same period last year.

• The main reason for the current uptrend comes from the biggest-weighted Food and Non-Alcoholic Beverages index with a 7.1% annual increase. Furthermore, nine (9) out of the eleven (11) commodity divisions were cited to have posted higher annual increases during the month of July.

• The Food Alone index was higher at 6.8% in July 2018 compared to 5.8% last June and 2.7% in July 2017.

• Inflation in the National Capital Region (NCR) was also higher at 6.5% in July 2018 compared to 5.8% last month and 2.9% last July 2017. For Areas Outside NCR (AONCR), inflation increased by 5.5% in July 2018 compared to 5.1% this June and 2.2% the same period last year. These point to a consistent uptrend seen in the level of prices.

• Current headline inflation may mean that the worse is not yet over. However, looking at core inflation, a good indicator of long-term inflation trend, it seems that the probability of inflation further increasing is lower. Core inflation has accelerated by 4.5% in July 2018 compared to 4.3% and 2.1% in the month last year; but month-on-month, core inflation may be slowing down.

• With this stronger-than-expected July 2018 inflation, will the BSP raise rates on August 9th, Thursday? The Economic Research Unit (ERU) thinks that BSP will definitely pull the trigger and will definitely follow through with a “strong response” to the tune of 50 basis points.

• Although much of the recent uptick on inflation are largely attributed to supply-side issues, ERU sees that the “strong response” by the BSP may be principally directed to the market and its inflation expectations, with the end of “firmly anchoring” said expectations. On the other hand, addressing the heightened level of prices per se should be channeled and directed by tweaking general economic policies that can probably cure certain market inefficiencies that are showing amidst the country’s economic expansion.

Outlook by Ruben Carlo O. Asuncion, UnionBank's Chief Economist

Note: Any opinion or statement in the Philippine Outlook does not constitute the opinion of UBP. Your use of this document and any of its contents is at your own risk and UBP does not accept any liability for the results of any action or decision taken on the basis of or reliance on the Philippine Outlook or any of its contents.

Posted by

UnionBank PublicationWe are a team of professionals providing relevant content to startups, micro, small and medium enterprises.

View UnionBank 's profile

Most read this week

Trending

Learning & Development 60 week ago

Comments

Share this content

Please login or Register to join the discussion